- World of DaaS

- Posts

- Yext CEO Michael Walrath

Yext CEO Michael Walrath

Software Consolidation and Convergence

|  |  |

Michael Walrath is the chairman and CEO of Yext, a publicly traded digital presence platform. Prior to Yext, Michael cofounded Right Media, the first at-scale digital ad exchange, which was acquired by Yahoo in 2007.

In this episode, Michael and Auren discuss:

Software vendor consolidation

Changing attitudes around growth vs profitability

New dynamics of VC funding

Running board meetings as a CEO

The Proliferation and Consolidation of Software Vendors

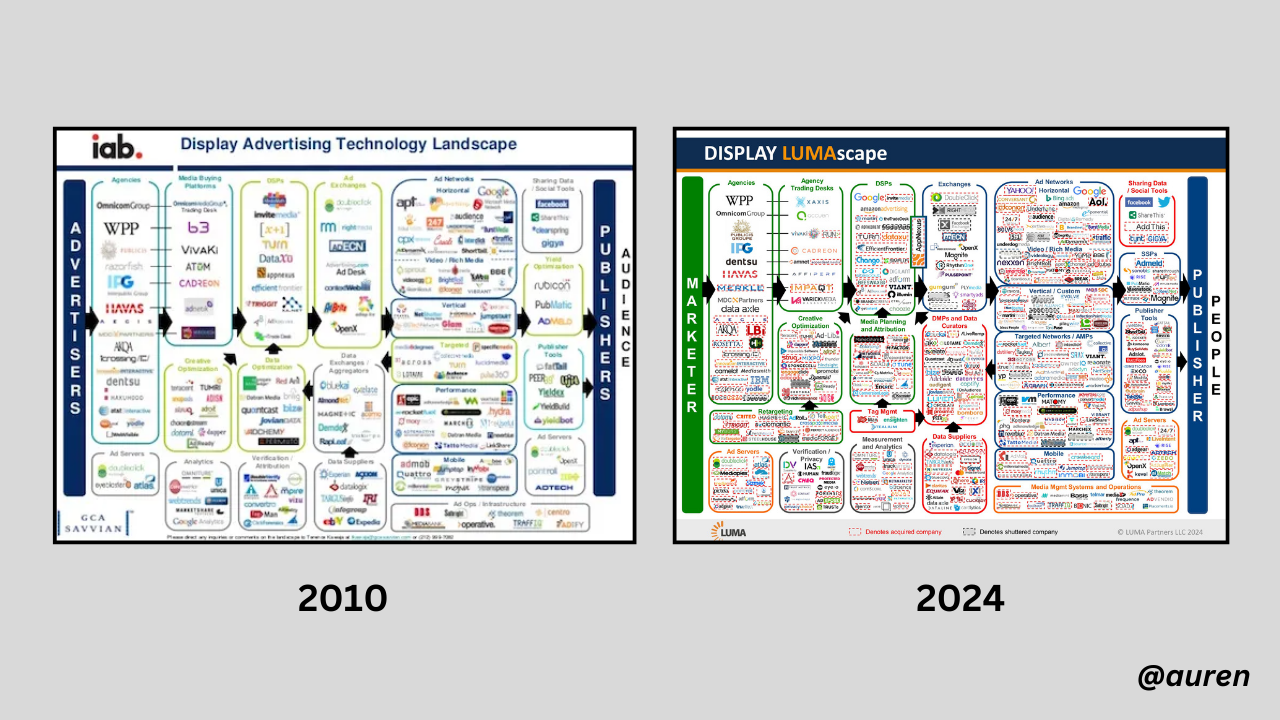

Walrath begins by highlighting the dramatic increase in software vendors over the past decade, from about 200 in 2009 to approximately 14,000 today. This explosion in vendors has led to companies using an overwhelming number of software solutions, often resulting in inefficiencies and redundancies. However, Walrath predicts a shift towards consolidation in the near future, driven by budget constraints and the need for more integrated solutions.

NOTABLE QUOTES:

"If I can put myself in a mindset where I think in terms of five or 10 or 15 or 20 years, then, you know, what happens this quarter, what happens next quarter is so much less important than exceptional execution over time."

“If you can get profitable, then as a software company, you basically have forever to figure out how to get a growth engine going again.”

“We are very much moving back towards how efficient can we be and how much of our effort converts into thrust. And I think it completely changes that conversation from size is good."

Adapting to a "Gravity Environment"

The tech industry has experienced a significant shift from what Walrath calls a "zero gravity environment" to a "gravity environment." In this new landscape, companies must focus on efficient execution and capital allocation rather than pursuing growth at all costs. Walrath emphasizes the importance of thinking in terms of decades rather than quarters, and making strategic decisions that create long-term value.

Challenges of Running a Small-Cap Public Company

Walrath discusses the difficulties of managing a small-cap public company in the current market environment. He notes that while Yext is now more profitable than it was five years ago, its market valuation is significantly lower. This paradox highlights the changing priorities of investors and the need for companies to adapt their strategies accordingly.

it’s getting crowded out there

Capital Allocation Strategies for Tech Companies

As Yext generates substantial cash flow, Walrath outlines several approaches to capital allocation:

Accumulating cash on the balance sheet for future opportunities

Investing in organic growth through product initiatives, sales, and marketing

Pursuing strategic acquisitions to expand offerings and consolidate market share

Returning money to shareholders through dividends or stock buybacks

Walrath emphasizes the importance of disciplined decision-making in each of these areas, always considering the long-term impact on shareholder value

The full transcript of the podcast can be found below:

Auren Hoffman (00:00.11)

Hello, Data Nerds. My guest today is Michael Warath. Michael is the chairman and CEO of Yext, a publicly traded digital presence platform. Prior to Yext, Michael co -founded Right Media, which was the first at scale digital ad exchange, which was acquired by Yahoo in 2007. He's also done a whole bunch of other amazing things in the tech world and even in golf too.

Michael Walrath (00:03.126)

Yeah, yeah, of course.

Ready.

Auren Hoffman (00:28.995)

Michael, welcome to World of DAAS.

Michael Walrath (00:31.242)

Thanks, Auren. It's great to be here.

Auren Hoffman (00:33.122)

Really excited. Now the number of software vendors has been increasing dramatically like over the last couple decades. Are we going to see more software vendors continue or are we going to see more vendor consolidation?

Michael Walrath (00:47.64)

Wow. We go right into predictions. Yeah. So it's a, we, when we started Yext, we counted, you know, and I, we've kind of gone back and looked at this. was something like 200 vertical software vendors selling to, you know, front office. call it kind of the CMO or the CMO CIO combo. today we count about 14 ,000. and so yeah. And I'm talking like 2009 to, you know, to

Auren Hoffman (00:49.74)

Yeah.

Auren Hoffman (01:10.638)

Wow, 200 to 14 ,000. Yeah, yeah, that sounds about right. Yeah, yeah.

Michael Walrath (01:17.512)

today. And like we can unpack, we could probably spend the whole time talking about why that's happened. But, you know, I think there are myriad impacts to that, some of which are just, yeah.

Auren Hoffman (01:29.71)

Well, let's, let's, I would love to get your, mean, it's, it's easier to sell to, to software, you know, back in the day, maybe you'd have to sell something. was like a $3 million implementation to make it make sense. Now you can say, start with like a $3 ,000 thing, right?

Michael Walrath (01:45.024)

Right. Yeah, totally. Yeah, I think that was the whole software is going to eat everything and I think it did. Right. And I think, you know, easier to input easier to use less capital cost up front all those all those things.

Auren Hoffman (01:57.87)

And that also means like before the average, one of these companies may have had six tech vendors and now they have 60 type of thing or.

Michael Walrath (02:07.64)

I think, yeah, 60. I wish I had 60. One of the first things I did when I got here as CEO, I've been here for 15 years, so it's ultimately my problem no matter what. when I took the CEO job, I asked the team to give me an audit. I had a whole list of requests. One of them was give me an audit of how many software vendors we're using. And the number was like 120. you started to... Yeah, until you start to get into the details and you realize like, okay, we're using...

Auren Hoffman (02:10.05)

Yeah.

Auren Hoffman (02:27.298)

Yeah. Yeah. Yeah. That sounds pretty normal. Yeah.

Michael Walrath (02:36.876)

This one for CRM, we're using this one for sales planning. We're using this one for prospecting. We're using this one for marketing. And you start to go, okay, we seem to have like seven or eight of these that are all just being used by the sales team.

Auren Hoffman (02:47.906)

Yeah. And you got like a LinkedIn subscription and these ads over here and you know, all this other stuff.

Michael Walrath (02:53.368)

It's like, yeah, you're using Salesforce, you're using Clary, you're using like, and that's just on the selling side, right? In the marketing side, there's a whole nother piece of it. And so that's how I...

Auren Hoffman (02:58.798)

Mm

Totally. Yeah, yeah, like a payroll vendor and just all the stuff,

Michael Walrath (03:07.638)

Yeah. And when you realize and then you start, if you really start digging into it, you start realizing is that you, you, you, need more than one, right? You know, but you, you know, for any given thing, but you don't need seven. And the, part of the reason, look, this is, I think this is all like well intentioned, right? A lot of companies got funded, money was free. there were a lot of needs and, and it became, you know, being verticalized became, was the hot thing, right? There's a period from

Auren Hoffman (03:19.426)

Mm

Michael Walrath (03:34.648)

2010 to 2015 where if you weren't verticalized, you couldn't get funded because it was like, no, have to, you know, the, sort of conventional wisdom of the early stage investment community was you, you have to be incredibly verticalized so that you can own a little vertical. that's why now, like what we're seeing today is that those businesses are really struggling in this environment because finally money isn't free. And, and the, and, and the other big part of this that has to be talked about is that, you know, this was the

12 years of the digital transformation, right? So you had, you know, highly elastic and nearly unlimited budgets classified under, you know, large enterprises undergoing the digital transformation. COVID accelerated that, right? And so we, you know, we saw what happened with the combination of ZERP and COVID and the digital transformation. And so, so I think what people in a lot of cases are struggling with is understanding like, why is everything that worked for 12 years not working anymore?

And a big part of it is that it's way too fragmented. And as the CMO for the first time in, you know, probably two years ago, the CMO for the first time in 12 or 14 years, you know, was, was hearing from the CFO, Hey, I'm not giving you unlimited increase. You don't get a 20 % increase or a 15 % increase or a 30 % increase this year. You got to hold your budget flat. and you have to potentially reduce some headcount. And all of a sudden it's like, well, how am going to manage a hundred software vendors?

with less money and less people. And so this is where I, what I think we're seeing as a macro shift is if I'm a CMO, a CIO, a CFO, I'm starting to think about, I have fewer people doing more work. Fragmentation is happening everywhere and I I need to consolidate what's happening. So yeah, the very long answer to your question, which really just required a, are we going more fragmentation or are we going consolidation? I think we're going consolidation.

Auren Hoffman (05:31.054)

Just and obviously not going back to, you know, 2009 time frame where there were, we're not going from 14 ,000 back to 200, but we might be going 14 ,000 to 10 ,000 or, know, how do you think of it?

Michael Walrath (05:45.272)

Yeah, I mean, the question is how many of those 14 ,000 are actually still alive, right? So when you couple the fact that we've had this massive proliferation of, you listen to enough podcasts, these numbers start to float around in your head, right? So I forget who, maybe it was on the all -in guys were talking about this a couple of weeks ago, you know, 1400 software unicorns, right?

private software unicorns that raised at over a billion valuation, right? So 10 % of the, you know, what we're using that number of the software market are private companies that have raised it over a billion valuation, right? How many of those companies actually like will go public, right? And was that, that was the discussion that I think they were having and I, knows, right? But lately the answer is close to zero. It rounds to zero, right?

Auren Hoffman (06:23.534)

Amazing. Yeah.

Michael Walrath (06:37.464)

But I think the bigger question is how many of those companies actually still have a business, right? Are still operating, a growing business or even a business that's not sort of declining. And the capital markets are pretty close to most of those businesses. So that tells me that it's probably not 14 ,000 to 10 ,000. It might be 14 ,000 to 7 ,000. It might be 14 ,000 to 5 ,000 over time.

partly because broader platforms make the world much better for the marketer in a lot of ways, but particularly in an AI world.

Auren Hoffman (07:15.086)

There's also this weird thing where to sell, if you're doing enterprise sales, it's super expensive. You have to hire these expensive salespeople and just takes a really long time. have to do a lot of sales and marketing. So you have to raise all this money to go do that. And then of course, if it's really expensive to sell them, you have to charge a lot because the selling costs are so high. And so you have to charge a lot more than it is. And so you have all these companies kind of got like in kind of in that zone.

Michael Walrath (07:35.34)

Yeah. Yeah.

Auren Hoffman (07:45.206)

you every once in a while, like, I mean, we buy a lot of software sometimes from like, it's like one guy or one gal company, or maybe like three person company, and they don't, you just kind of like, go log on their site, somehow you find it, you log on their site, and you just pay in credit card, it's super cheap. And they're doing incredibly well, you know, they've got a multimillion dollar business, they're doing incredibly well for themselves, they've never raised much. And there's so many on that side. And it seems like though the number of vendors there is just

Michael Walrath (07:58.924)

Yeah.

Yep. Yeah. Yeah.

Auren Hoffman (08:14.638)

keeps going up. Maybe none of those businesses are ever going to be $100 million, $200 million businesses, but a lot of them can scale to $20 million and do incredibly well for the owners.

Michael Walrath (08:15.798)

Yeah.

Michael Walrath (08:24.342)

Yeah. Yeah. Yeah, no, that and I agree. think that's a big that's a part of it. Right. And I actually think that's a lot healthier because those tend to be product growth companies. They tend to be the companies you find through referral. They have CAC ratios and things like that that make sense because they're not they don't you know, they're not supporting a big enterprise sales team and and things like that. So so we the ones that I, you know, I'm more focused on because we we do tend to sell into larger enterprise.

are the ones that have bought, who've kind of drank the Kool -Aid around, know, growth at all costs is the only thing that matters. You can spend unlimited sales and marketing dollars and unlimited R &D dollars as long as you're getting the growth because at end of the day, that's what market valued for a very long time. I mean, it's an unprecedented thing that we had like 12 years where, you know, the only real mechanism for valuing software companies, you know, scaling software companies was growth.

Auren Hoffman (09:10.807)

Yeah.

Michael Walrath (09:23.64)

Right. And so I don't know how many of those 14 ,000 are those healthy kind of PLG type companies. I think it's probably a significant number. And I think they're a lot less exposed because like you said, they're profitable. They make money. They're not trying to.

Auren Hoffman (09:38.498)

Yeah. Or even if they're not PLG, maybe they've got some service side or something like that or whatever. They're good businesses.

Michael Walrath (09:42.902)

Totally. Yeah. Yeah. Yeah. We work with a lot of those companies on the reseller side of our business and, they do an amazing job servicing the SMBs and bundling and packaging things together. And in a lot of cases, they have some home built software and then they are OEMing our software in. It's a great deal for us. And I think it's a good deal for them too, because, you know, it would be a massive investment for them to build what we've built. But it would also be a massive investment for us.

to sell to those tens and hundreds of thousands of smaller businesses. So those type of economic structures I think work really well.

Auren Hoffman (10:18.776)

Now every year there's someone who's predicting like massive consolidation. You know, you see these kinds of crazy logo slides, let's say in Mark Martek or ad tech kind of world. And every year someone's saying, we're going to have so much consolidated. And then, and then the next year the slides get even crazier and crazier. Like it's, but at some point, like you reach a point that can't get more crazy. Like it does, you know, so.

Michael Walrath (10:23.405)

Yeah.

Michael Walrath (10:35.244)

Yep. Yeah.

Auren Hoffman (10:42.51)

That's what you're saying. It's like, okay, we just like, I'm just finally, calling peak or L now, like I'm finally calling the craziness right now.

Michael Walrath (10:49.526)

Yeah. Well, yeah, I mean, I think I figured out that like making bold predictions like that is just a bad idea, right. Which which hasn't really necessarily stopped me. think, you know, I've been a little more bearish probably than most of my most of my peers overall. And I think some of that bearishness is just seeing the unsustainability of some of these, you know, some of these financial models and inside software companies. And so, you know, I'm not necessarily predicting that there's going to be a massive wave of consolidation.

I just think there's going to be pressure across the board and companies who understand that breadth wins in an environment where the budget is constrained in any way. Breadth wins because you can bundle and package smaller competitors out of the market.

That I think is a trend that we will continue to see as long as there's pressure on the budgets of the enterprise, which I don't personally think is going to obey it anytime soon.

Auren Hoffman (11:56.846)

And what is going to like you mentioned all these companies, there's so many companies out there that have raised, say $100 million or even more than that. They're doing well. And a lot of them now have found a way to get their profitability. But they're definitely not worth what they raised it at. They may have raised a hundred and now they're worth 150 or 200 tops. And they can't really sell the company because then, then, you know, with the pref stack, the founders won't really make as much money. So they just kind of like keep going.

Michael Walrath (12:03.212)

Yep. Yep. Yeah.

Michael Walrath (12:11.894)

Yeah.

Michael Walrath (12:16.514)

Yeah, yeah.

Michael Walrath (12:26.199)

Yeah.

Auren Hoffman (12:26.222)

keep compounding and if they keep compounding enough, then maybe, maybe, with the pref stack, you know, it works. Is that just what's going to happen? They're just going to keep like building the business slowly.

Michael Walrath (12:37.208)

Yeah, I mean, I think we're seeing different approaches, right? So I actually, I were advising that kind of private 100 million ARR company, what I would advise them is get profitable, right? And control your own destiny. The market will not, your investors are very unlikely, especially if your growth is slowing, which it's all slowing, right? mean, think, yeah, a year and a half ago, there were, we look at our public, like Pierre said, and

Auren Hoffman (12:57.91)

Yeah, everyone's song. Yeah.

Michael Walrath (13:06.2)

There are like 40 or 50 companies who we kind of track there. you know, a year and a half ago, two years ago, probably more than half of them were growing at over 30%. Now I don't think there, I don't think there's a single company in that group that's growing at over 30%. I was talking to a, an investor of ours, really smart investor of ours has been investing in software for a really long time. And he said something I thought was really interesting. said, look, 20 years ago, a company that sustained growth at 30 % for any period of time was a unicorn.

It was a total outlier. And what we've seen over the last 10 years is that if you're not, that it was, it was like the minimum bar, right? If you're not, if you're not 30 % growth or higher, you're just, you're. Yeah. Well, rule. Yeah. And look, I think rule of 40 has a, has a lot of merit. Sure. Yeah. Or, 10 growth and 30, you know, you've been like, yeah, that's a great company. And, and historically that was a company that, know, that the market really valued because.

Auren Hoffman (13:45.038)

Yeah, this rule of 40 idea.

Auren Hoffman (13:50.862)

Cause it could be 20 EBIT and 20 growth or somewhere or 10 growth. Yeah. Yep. Yep. That's a good company.

Michael Walrath (14:03.224)

You compound 10 % growth and 30 % EBITDA over 10 years and you create a ton of value, right? We went through a period for 10 years where just that whole notion of there are different ways to create value went out the window. It was only one of those metrics mattered and it was the growthy one. So anyway, you had.

Auren Hoffman (14:07.458)

That's amazing. Yeah. Yeah.

Auren Hoffman (14:17.197)

Yeah.

Auren Hoffman (14:20.814)

Yeah. And if you're growing at 40%, but you're negative 25 % e -bit or negative 30 % e -bit or something like that, which, know, sometimes the negative like a hundred percent, then it's a less good.

Michael Walrath (14:27.575)

Yeah.

Yeah. Yeah. Well, it's it. Yeah. And look, we all understand why that happened, right? When money was totally free and your next round was, you know, we saw this in for a shorter period of time in the late 90s, where the next, you know, it was all just how fast can you get to the next round? Right. I think we saw that for in this world for a much longer period of time. And what were but but those companies who you are talking about, those 50 million are our 100 million are our companies. They've all seen their growth slowing to.

Auren Hoffman (14:46.209)

Yep.

Auren Hoffman (14:59.598)

Yes. Some of them negative growth. They're still good businesses though. They have a good product, people like it, and maybe they're going from 100 this year to 99 next year or something, but they're profitable and they're fine. They're just never going to hit the valuation metrics that they once raised at.

Michael Walrath (15:00.057)

It's harder to sell. It's Yeah, yeah

Michael Walrath (15:15.522)

Totally.

Michael Walrath (15:22.102)

Yeah, or they'll have to or they or they have to like they have to find a way to restart the growth engine in a meaningful way to you know, so this I think then this comes down to our we have a tendency to take very short lenses, right. And so so if you can get profitable, then you as a software company, you basically have forever to figure out how to get a growth engine going again. Right. Now, your investors don't want it to take forever.

Auren Hoffman (15:40.888)

Yeah.

Michael Walrath (15:51.66)

And if you're public, they certainly don't want us to take forever, which is part of the thing that I think we've struggled with, you know, in terms of, you not, not, not in terms of what I think is fundamental value creation, but in terms of perception. So, so my advice to those companies has always been, and I, and we've invested in a bunch of them, you know, get profitable in this type of an environment. And then you have all sorts of options. I think what, a lot of cases, you know, founders and CEOs and teams are learning the hard way is that.

Auren Hoffman (15:55.254)

Yes, yep.

Michael Walrath (16:22.433)

you could logically see your way to a down round. And I think it's really hard for folks who haven't been through one of these cycles to understand that the down round is actually probably the worst thing for your investors. It's actually probably worse than an exit at less than the preference stack. Because I think a lot of investors would rather, and maybe this is a controversial point of view, but they would rather

Auren Hoffman (16:40.995)

Yep.

Michael Walrath (16:51.256)

take 50 % of their money back now, then have to mark their investment down 50 % and have that hit their unrealized returns. so part of what we've seen talking to founders is they assume that, well, I raised my last round at a half a billion valuation, I can always raise money at two or 300 million to bridge and they can't, right? Because the investors would rather sell the company for $100 million for capital raised.

then let you raise at 250 or 300.

Auren Hoffman (17:22.894)

Yeah, yeah, exactly. The and it's also a it's like there's certain personality types of CEOs. And if you're not growing that much, and let's say you're, you know, you're burning 500k a month, even if you have $20 million in the bank, okay, well, okay, that's gonna take a long time. got three years of runway or something. But like, you know, if you're not growing, there are certain types of CEOs is like, great, like I'm gonna

I'm making the cuts now. And then once I figure out the growth engine, I'll reinvest. And there's other ones like, well, I've got these 20 side projects. I know it's going to happen. know the growth is going to happen. I'm going to keep it going. And I'm not going to make the tougher decisions. Like, there something like you could know, like by meeting with CEOs that they would be one type of personality or another, like, could we give them a personality quiz or something?

Michael Walrath (17:56.78)

Yeah.

Michael Walrath (18:17.738)

Yeah, maybe. mean, that's probably, you if investors were actively investing right now, that's probably the sort of thing they'd want to do. But it's interesting. You don't see a lot of funding is happening. And I think it's.

Auren Hoffman (18:28.056)

That's right. Yeah, these are people who raised money a long time ago. They just may have a lot in the bank.

Michael Walrath (18:30.808)

Yeah. Yeah. You know, I think one of the things and I think about this a lot because I've been because I'm old now. Right. So I've been I've been around for a long time. And this will be the third downturn cycle that I've you know, my first one was I started working at DoubleClick. Yeah, we're the same. Yeah. Yeah. Like we are lucky because basically I entered the workforce in 1999. I went to I had a sales job at DoubleClick. I was 24 years old.

Auren Hoffman (18:47.244)

Yeah, we're like same age, same kind of vintage. Yeah.

Michael Walrath (18:58.297)

And that stock went up $20 every day. And I got a couple thousand options and I was like, this is perfect. I'm going to be a millionaire, right? Stocks at $200. I'm going to, it's going to go to $500 and I'm going to be a millionaire just off this. And, and, you know, that all ended very, very quickly. And I think in my first two years there, there were nine rounds of layoffs. There were like, you know, it was unbelievable. You know, it was an unbelievable experience, but like, and I'm sure, you know, you like, we were both living through the same world at that point.

What it created in me was a sense of like, okay, this is what happens in downturns. And then I had, and then I started right media in late 2002. There was no, mean, there was basically like one VC in New York. was Fred Wilson and he invested in consumer. So there was nobody to talk to. found Jonah No Goodheart, who were my customer at DoubleClick and they funded the company. you know, they, they wrote the first check into the company, but, but all that did was give us six months, run six months, a runway. So

Auren Hoffman (19:41.059)

Yeah.

Michael Walrath (19:56.152)

We had to figure out how to make money and we had to figure out how to, you know, reinvest the cashflow into growth. And if you think about it in tech, especially that was the last time 2003, 2004 was the last time that like the market required that you an efficient growth model, because by 2005 we were ripping 2008 was a, was a speed bump for tech. And then we caught the digital transformation wave and it's been, you know, it's been just an enormous party sense until.

we hit the end of 2021 and this hangout, know, and I think I'm not, think the party is officially over and the hangover is bad. but, the crazy thing is inside the company, we've got people, you know, who, who've been in the workforce for 20 years, who had never been through a layoff. They never experienced it before. and so I think that's why this is such a difficult time for a lot of people because the party was so long.

Auren Hoffman (20:44.301)

Yeah.

Auren Hoffman (20:50.368)

Yeah, that's really interesting. What else has changed about running tech companies over the last couple of decades?

Michael Walrath (20:56.28)

Everything and nothing. I think the longer lens we can take, the more value we're going to create. And so I've kind of belabored the point that I think we got really myopic about a single metric over the last 15 years. I think growth, just growth.

Auren Hoffman (21:00.406)

Hahaha

Auren Hoffman (21:17.398)

Just growth. Everything was just so focused on growth.

Michael Walrath (21:20.152)

Growth. mean, there was a point I'm going to pick on ourselves, right? There was a point and it's my, was the chairman of the company, so it's on me, right? But in, I think it was in 2020, maybe it was 2019. We were spending 74 % of our revenue on sales and marketing. and we were declining growth. And the answer, the default answer inside the company was, well, the only way we're going to get more growth is to spend more money on sales and marketing.

Auren Hoffman (21:40.13)

Yeah. Yeah.

Auren Hoffman (21:49.549)

Yeah, yeah.

Michael Walrath (21:50.144)

Right. And, and, and, you know, in a lot of ways we all bought into it and like, I should have known better, right? Like we all should have known, we all should have known better.

Auren Hoffman (21:56.108)

Yeah, yeah, totally. I've made, I've made that. The problem is I've also, I've made that exact mistake like five times in my life or something. You know, it's like, you would think you would learn after the second time or something.

Michael Walrath (22:02.06)

Yeah. Yeah.

Michael Walrath (22:07.736)

Well, and look, if we were public, the market was only paying for growth. was better to be highly unprofitable and growing 25 or 30 % than it was to be highly profitable and growing 10 or 15%. And, but, there were so many like myriad, just terrible consequences of making those types of decisions. For example, we had twice as many salespeople as we should, as there was availability of market opportunity there. So, so

Auren Hoffman (22:11.405)

Yep.

Auren Hoffman (22:35.757)

Yeah.

Michael Walrath (22:36.472)

What happens in that scenario is your best salespeople. Yeah, they will. killing each other. There's not nearly enough to go around and your best salespeople go. And by the way, this is in 2020 and 2021 when like, you know, Google and data dog and MongoDB and everyone who's thriving, they might as well have been having like they're, all within, you know, basically like a stone's throw of our office. Yeah. Yeah. And so, so, you know, if you have a time machine,

Auren Hoffman (22:38.04)

They're hurting each other. Yeah. Yeah. Yeah.

Auren Hoffman (22:50.947)

Yeah.

Auren Hoffman (22:55.906)

Yeah, they're going to go somewhere else. Because they're not getting the leads that they need.

Michael Walrath (23:05.464)

Right. You go back in time and you disregard the fact that the market is only paying for growth. And you say, look, over 10 years, the right answer here is instead of having 200 salespeople, I should have 50. Those 50 should be the best. They should make amazing compensation. and, know, and then there will be enough demand to go around. That might mean we only grow at 10%, but actually will be, you know, you're much more likely to be a rule of 40 company growing 10 % and having 30 % margins in that scenario than you are.

Auren Hoffman (23:17.43)

Yep. Yeah.

Michael Walrath (23:35.399)

And that was just a little bit of a unique quirk to our business.

Auren Hoffman (23:37.262)

By the way, I have, I have found across the board of almost every company that we've been kind of double clicking into that almost every company has like, like two X three X four X more salespeople than they should have. like if you look at the salespeople's calendars, like your bet, the best salespeople are just not busy enough. I'd rather pay the best salespeople twice as much, but have, have a 25 % of the salespeople.

Michael Walrath (23:49.602)

Yeah, yeah.

Auren Hoffman (24:04.46)

make them super happy, make them super, their close rates are gonna go up. they're gonna be, you give your best leads to your best people, then just kind of like more spread the peanut butter thing.

Michael Walrath (24:11.842)

Totally.

Michael Walrath (24:15.864)

Yeah, and it's spreadsheet math, right? So it's really easy to make it work on paper, right? I have 200 salespeople and they're booking $400 ,000 a year each, which is a terrible sales productivity. Terrible, terrible. But...

Auren Hoffman (24:18.647)

Yeah.

Auren Hoffman (24:28.088)

That'd be terrible. Yeah. my gosh. If you had a salesperson book 400K a year, this is like very hard to make money.

Michael Walrath (24:34.68)

Well, yeah, I mean, you're paying them that much money, right? So forget like overall cost of acquisition. So just I'm making those numbers up. But if you're in that scenario, it's really easy to build a spreadsheet which says, well, hey, like, if growth is the only thing that matters, if I had 400 salespeople doing $400 ,000 a year in sales, then I would at least be doing double the bookings and my overall ARR and revenue growth would be higher. And you can actually convince yourself that that will work.

Auren Hoffman (24:37.57)

Right, right.

Auren Hoffman (24:57.217)

Right, right.

Michael Walrath (25:03.288)

But what it actually what it does is, know, so doubling the sales team there, what you see is, well, you know, the most likely scenario is that they're going to do 200K each in bookings. Right. But actually, it's worse than that because because the best ones leave and you you wind up with 400 doing 150 and you're now you're just in a death spiral. Yeah.

Auren Hoffman (25:15.756)

Yeah.

Auren Hoffman (25:21.646)

Or no, even if the best ones don't leave, they your close rate starts to go down pretty dramatically because they're not getting the good leads. So if your close rate was 10 % before now, your close rate is going to be 5 % overall, it just becomes so it is a little bit of a spiral.

Michael Walrath (25:37.656)

Yeah. And so, I mean, I think you asked the question like what's changed. think what has to continue to change. The market is applying gravity to a, know, for the first time in, you know, starting in, you know, a couple of years ago, for the last two years, we've been feeling gravity for the first time in, you know, 12 plus years.

And so as management teams, think it's, it's, have to shift from a zero gravity environment to a gravity environment, which, you know, I'm not an astronaut, but like I've heard that makes you sick, right? That makes you feel. And that's what we have is we have a lot of people who are feeling sick about the fact that like all the rules have changed and all the things that work so well for, you know, a decade just or longer just don't work as well anymore. people, you know, I don't, not everybody loves this, but

Auren Hoffman (26:12.493)

Right.

Yeah, yeah, yeah, I love that analogy.

Michael Walrath (26:34.538)

I love this environment. I think this is the environment where

Auren Hoffman (26:39.246)

Well, you're like, you're more of a wartime CEO.

Michael Walrath (26:43.384)

I just would rather be in an environment where great execution is differentiated. And I think and if you can look, this is hard. I struggle with this every day. If I can put myself in a mindset where I think in terms of five or 10 or 15 or 20 years, then, you know, what happens this quarter, what happens next quarter is so much less important than exceptional execution over time. And

Auren Hoffman (26:47.842)

Yes.

Michael Walrath (27:13.564)

you know, and judging the environment correctly. And so that is why I like this environment is I think it forces you to think really carefully about what's available and what's not available.

Auren Hoffman (27:24.91)

One of the that was happening before is you had these like, let's say 100 million ARR companies and they had like a thousand people. So it's like a, you know, a hundred K ARR per person or something. And then they then they would eventually go to 200 million ARR and they would have even more than like 2000 people. Like they didn't get any more efficient over time. And you have this like

Michael Walrath (27:38.988)

Yeah? Yeah.

Michael Walrath (27:47.81)

Yeah. No. Yep.

Auren Hoffman (27:53.312)

One of the problems with adding more people is just the management goes up dramatically. Like you have this coordination problem internally that becomes really, really hard to deal with. it's one of the nice things about being more lean is it's just easier. You don't have to be like the world's best manager anymore to manage a company as it grows.

Michael Walrath (28:18.36)

Yeah. I mean, think, you know, we talked about, I mean, we talked about the sales productivity and those expenses and things like that, but there's also just, there was this, you know, we just went through this weird period where like, it became really important how many people were in your organization, right? We would interview people. And by the way, we were losing, you know, there was a period where I think we were having like 40 plus percent annual attrition because people were going to the data dogs and the Googles and we'd have, you know, you'd have

Auren Hoffman (28:34.838)

Yeah.

Auren Hoffman (28:43.852)

Yeah, of course. Yeah. So then you have to they have to a huge recruiting engine all the time. And then people have to spend all their time interviewing people to that's that's a huge time waster if you have to spend like half your day interviewing people.

Michael Walrath (28:49.516)

Yeah.

Totally.

Michael Walrath (28:57.24)

Yeah, there was a year where we hired like 600 people and grew the company by 50 heads. Right. It was like, mean, it wasn't 600 people out of 10 ,000. was like, you we had, we had, you know, 1300 people, we hired 600 and the company grew from 13 to 1350. Right. And yeah, that was, you know, that was just the war for talent. Right. And what was it to me, what was interesting about that time is you would talk, you knew, so we're interviewing constantly.

Auren Hoffman (29:01.111)

Holy mackerel.

Auren Hoffman (29:06.36)

Yeah.

Auren Hoffman (29:14.38)

Yeah, because you have a lot of people leave.

Auren Hoffman (29:19.458)

Yeah.

Michael Walrath (29:25.72)

Right. And I've had to kind of rebuild the management team in a lot of ways here. And, and you saw over and over interviews, what you'd hear people talk about as well. You know, I, I managed an organization of 500 people. Right. it became a thing that, you know, well, yeah, the LinkedIn profile says this company has 1200 people or 1500 people or whatever it is. And we got, we got so enamored with, with all types of growth. Right. How big is my organization? How many people do I manage? How many VPs work for me?

Auren Hoffman (29:45.048)

Yep.

Auren Hoffman (29:49.804)

Mmm.

Michael Walrath (29:55.14)

And all of that is this like incredible weight for an organization to carry. It's a compensation problem. It's a silo problem. It's a communication problem. It's all those things. We, we, we are very much moving back towards how efficient can we be and how much of our effort converts into thrust. And I think it completely changes that conversation from size is good.

Auren Hoffman (30:19.758)

I remember being kind of in this vortex just a few years ago in 2020 and just really starting to scale up. And the whole time I'm back in my head, I'm like, I know this is a bad idea. Like I know I can't absorb all these new people right away. Like I know we probably don't need all these people in marketing or something like, but like, I don't know if somehow I did it anyway. Like, I don't know why I did all these stupid things. Like it, it it seemed like, like somehow we just had this collective.

like stupidity that hit all these founders and CEOs at one time.

Michael Walrath (30:52.866)

Well, look, was everywhere. I'm not an economist, but underneath it all is the economy of growth. So money didn't cost anything. We had to go get growth. Venture investors, private equity investors, everyone had to deliver returns and had to deliver growth. And it just works so unbelievably well for so long. As long as I'm growing, I can sell it to the next guy.

Auren Hoffman (30:55.276)

Yeah.

Michael Walrath (31:21.08)

And the next person can build their pro forma that says this thing will grow like this forever. And then there'll be someone else who will pay for that growth. so we got in this moment where was like, we took as like just religious truth that 10 times ARR was what a company was worth. With no other question of like, well, how much does it burn? How much does it make? Like any of things, right?

Auren Hoffman (31:43.49)

Toy. Yeah, Right. Right. Exactly. Yeah.

Michael Walrath (31:47.768)

I don't know if there's, you know, there aren't very many trading for 10 times ARR, but it used to be like, it was just certainly in private rounds, it was just like, hey, that was the starting point.

Auren Hoffman (31:56.526)

Yep. Yeah. Yeah. Yeah. Exactly. And it kept going up. Like I remember we sold live RAM 2014. We got a little bit less than 10 X ARR, but we were, profitable and we're growing like almost a hundred percent. and then like, and then it's like, if we just probably waited two years, we would have got like 20 X ARR. yeah.

Michael Walrath (32:01.804)

Yeah. yeah.

Michael Walrath (32:12.78)

Yeah, yeah, they're good.

Michael Walrath (32:19.096)

for sure. Yeah. No, I mean, that's when we sold right media in 2007. I think we sold for 13 times revenue and like, you know, nine times a hour. And like, you know, I remember people, you know, getting phone calls like I cannot believe that. Like that's it's a crazy number. Right. And I felt like it was a crazy number. Right. I was like, how does anyone justify paying me 10 times, you know, you know, a hour? And like you said, five years later, it was like

Auren Hoffman (32:36.568)

Totally. Yeah, yeah, yeah.

Michael Walrath (32:49.403)

you know, the number would be two or three or four times that.

Auren Hoffman (32:51.726)

Yeah. Though today, I mean, we have one of our companies I've been involved with, like they're a good company. They're, you know, they're growing at 50 % per year. You know, they're, you know, a little bit more than five, 50 million ARR. They, they just, you know, they just did a raise at roughly 500 million. So they, they were able to command still that 10 X, and, know, not yet profitable, but, good company. so it still is happening like even like right now.

Michael Walrath (33:12.108)

Yep. Yep.

Michael Walrath (33:20.216)

Totally. Yeah, no. And look, 50 % growth on 50 million of ARR, that's impressive. Right? Like that's a company that is succeeding. And if you're not burning, you know, if you're not burning a ton of money to get that, that tells, you know, as an investor, and I've done a lot of this, you know, I would look at that company, I would say, okay, that is a company that has product market fit, that, you know, has some level of efficiency. And, you know, if they're, if they're

Auren Hoffman (33:23.84)

Yeah, it's pretty awesome. Yeah.

Auren Hoffman (33:29.688)

Too much, yeah.

Auren Hoffman (33:39.629)

Yep.

Michael Walrath (33:43.96)

If you're 50 million, you're growing at 50 % and you're burning 5 million bucks a year or even 10 million bucks a year, you're sort of in that rule of 40 category. Now, if it's burning $50 million a year to get that 50 % growth, think it's a completely different scenario. What I think has changed is that it didn't matter two, three, four, five years ago, if you were burning 50 million to get that 50 % growth, you still get that 10 times.

Auren Hoffman (33:51.651)

Totally.

Auren Hoffman (33:57.336)

That's a problem. Yeah.

Michael Walrath (34:13.944)

was indiscriminate kind of funding. And I think that's where the pain is in the market today is, you you can't afford to burn $50 million a year to grow 50 % at 50 million of ARR anymore. And people aren't going to fund that business.

Auren Hoffman (34:26.37)

Yes, makes no sense.

Now you were, you were chairman of Yext and then you became CEO. And so now you're in some ways, like, how do you, do you think about running your board meetings differently now that your CEO where you kind of like started on the board there, then you would like, if you just kind of like started as CEO.

Michael Walrath (34:48.92)

Yeah, I mean, it's certainly been an evolution, right? So so when I was when I was building right media and we raised our first round of institutional capital two years after we found in 2005, all of sudden I had to have a board meeting, right? The board meeting before that was me and Jonah and Noah having a conversation whenever we felt like we wanted to. Right. It was it was a private company that was owned by us. And so, you know, I was.

Auren Hoffman (34:51.416)

Yeah.

Auren Hoffman (35:04.216)

Toy.

Michael Walrath (35:16.92)

At that time, I was 2008 years old or something like that. And, you know, I had to learn how to run a board meeting. I didn't have a call, right? Like the Red Point guys were very patient. They were like, Hey, here's some decks, right? Cause I showed up to the first one. had no deck. Like I'm just talking right on the whiteboard, right? And they're like, yeah, you know, this is, is, know, we're going to need to do this a little bit differently. so, you know, having gone through that and then, you know, having gone to Yahoo and.

Auren Hoffman (35:23.532)

Yeah.

Auren Hoffman (35:30.45)

Yeah. Yeah.

Exactly.

Michael Walrath (35:45.048)

been part of a much, much larger organization and stayed there for a couple of years through a really turbulent time. I learned a lot about how those board meetings were run and things, know, and sort of how to operate at scale, which, you know, and then 12 years of sort of the, the X board and other boards. What, what I, what I think has changed most is, is that I think a lot more in the boardroom, the way I thought about the company before I had investors.

Right. And what I think is missing in a lot of cases in the boardroom is that really that ownership mindset that like,

Auren Hoffman (36:20.91)

strategic like product oriented like that type of thing.

Michael Walrath (36:24.95)

Yeah, like one of the things that that, you know, that I that I try to do in any boardroom is like, is inject this notion of like, what if what if I know we're not right, we're a public company, we have responsibility to our shareholders. We do have shareholders in the room, you know, of various sizes. What if this was a family business? How would we think about it if it was a family business? Right. And in that, you know, what that

Auren Hoffman (36:35.149)

Yeah.

Auren Hoffman (36:50.764)

Meaning like we have a very long -term horizon, that type of thing.

Michael Walrath (36:54.616)

And a responsibility to think about the value of every dollar we spend and to think about the balances between growth and profitability. so Yext has gone from being five years ago with one of those 30 % growers that was highly inefficient to a company that this year, I think our consensus estimates have us in the minus 1 % growth as we've gone through a lot of changes and shifts in our strategy.

Auren Hoffman (37:00.514)

Yes. Yep.

Michael Walrath (37:24.248)

So, you know, that's a huge difference. But, you know, that company five years ago that the market valued according to its growth profile had, you know, was burning cash. you know, our company, you know, will approach, you know, the next 12 months according to, again, I'm going to talk in terms of consensus numbers, something like $100 million of EBITDA, which translates roughly to free cash flow. like, when we look at that and you think about it, and I put the hat on and say, okay, if this were a family business,

Auren Hoffman (37:42.946)

Yeah.

It's amazing. Yeah.

Michael Walrath (37:54.392)

how much of that 100 million of free cashflow or EBITDA or however you want to think about it, would we invest in growth right now in this market? Because it's our money, right? And I think that is kind of the lens that disappeared in this kind of single mode market. But to me, it's the most important thing to bring into the room because it turns the conversation into a capital allocation and long -term value conversation instead of a

Auren Hoffman (38:03.5)

Yep. Yep, exactly.

Michael Walrath (38:24.342)

instead of a how do we get the market to react the way we want the market to react in the short term.

Auren Hoffman (38:30.744)

You know, in my entire life, being on boards, running boards, including my own boards, I don't think I've ever had like a great board meeting. like I've never, I've never been a board member of a great board meeting. I've certainly don't run great board meetings. Like what advice would you give to people like me who want to like a level up, who want my board meetings to be like much better.

Michael Walrath (38:52.374)

Yeah. You know, it's funny. I don't know that I would, I've been part of hundreds of board meetings and I would sort of agree with you that like, I'm not sure I've ever walked out of, well, that's not true. I have walked out of board meetings thinking, wow, that was a great board meeting. Usually that's when I've just delivered a whole lot of good news. Right? Yeah. Yeah. Those are, yeah.

Auren Hoffman (39:11.34)

Totally. Totally. I've been in those board meetings too. And it's like, yeah. Or being on the board and she was like, I have any advice? And you're like, no, you're doing amazing. Like, I can't do anything for you. Like maybe I should, maybe we should pay you more, but that's about it.

Michael Walrath (39:21.408)

Yeah, yeah.

Michael Walrath (39:26.41)

No, and I mean, you know, I think there was a period of time where right media board meetings were like that, Moat, which Jonah and Noah ran, but you know, I had the best job in that company too, chairman, non -executive chairman. know, I mean, tell you more than like right media and Moat, like we never had a bad board meeting because every board meeting was just a like, we're outperforming the plan. Everything's working. And also, you know, in our case, exactly. Yeah.

Auren Hoffman (39:32.492)

Yeah, what a great company. Yeah.

Auren Hoffman (39:47.502)

Hehehehe

Auren Hoffman (39:52.738)

Those mean the board meeting is that helpful? you know, it's like all the execs are there. They're spending three hours. Like, how are they really is a really good use of their time, right? Yeah.

Michael Walrath (39:57.004)

Yeah. Yeah.

Right. it's spending three hours high -fiving.

Auren Hoffman (40:05.718)

Yeah, I mean, maybe that's good. you know, mean, high fiving, like, you know, celebrating each other. It's not a bad idea either.

Michael Walrath (40:11.798)

Yeah. No, it's a good thing, but I think where the board meetings get really good is when we get some tension in the room and where there's some, you know, and what I would call a constructive tension, right around where we're getting pushed on, you know, are these assumptions that you're making and are these strategic decisions and ultimately are these investments that we're making? Are they smart investments, right, over the course of the long haul?

Auren Hoffman (40:20.429)

Yes.

Auren Hoffman (40:40.716)

Yeah. But it's true of any meet, not just a board meeting, but like any meeting, you know, is only good if there's some internal meeting, at least some tension, just like any any movie. You're not going to watch a movie with no tension. Like that would be a really boring movie.

Michael Walrath (40:41.864)

And yeah.

Michael Walrath (40:53.942)

Yeah. Yeah. No, that's right. And I think it comes back to, like, I think we're I do I think we're entering an era that like, when we talk about like, maybe this I'll make a prediction, which might be embarrassing, because this is recorded. So I think in three or four years, like, we might look at this and say, Okay, like, I suspect in three or four years, we're going to actually be in a really good place. I think

You know, that we get into the AI is going to be a huge tailwind. think it's going to be a massive software is going to be a massive beneficiary of all these things. But I, but I do think in that when the party is back on again in some form or the other, the companies that are going to be doing the best are the ones who took this time to inject a completely different notion of value creation into their DNA and, and effectively said capital allocation matters. It has always mattered. If you look at the, you know, sort of the

Auren Hoffman (41:39.459)

Yep.

Michael Walrath (41:46.466)

you know, the last couple hundred years of capitalism, the best performance over time were people who, you know, it's Warren Buffett, they know how to allocate capital, right? They know how to think in terms of decades. so, fantastic, amazing book. And the thing that's so amazing about it is that most of the people in that book I had never heard of, right? know, like they outperformed Warren Buffett, right?

Auren Hoffman (41:59.33)

Have you read The Outsiders? I love that book. Yeah, one of my favorite books. Yeah.

Auren Hoffman (42:10.454)

Yeah, yeah, totally.

Yeah, totally.

Michael Walrath (42:15.544)

Not many people have done that, right? He's a huge hero of mine and I think what they do is amazing. But yeah, that's a great, that's a book that tells the story of, you and I think it's incredibly instructive in this environment where every dollar that we spend is precious and has to have a return.

Auren Hoffman (42:33.502)

There's a lot been written and talked about these smaller mid cap public companies, put Yext and that bucket there. From the outside, it seems very, very hard to run these companies as public companies. What is your advice to other CEOs going through it? And maybe your advice is to not do it, I don't know. But what's your advice to other CEOs going through all that stuff?

Michael Walrath (42:42.38)

Yeah.

Michael Walrath (42:58.1)

Yeah, I I think it's a I'm not sure that in my lifetime, I'm not sure it's been harder to be a small cap public company, partly because I just think the market doesn't care. Right. So so what's interesting is the extra was a mid cap public company when it was half its size and way less and way less profitable. Right. So so yeah, you go back five years. We were literally less than half the size.

Auren Hoffman (43:13.804)

Yeah.

Auren Hoffman (43:19.108)

huh. Yep. Back in the day. Yeah. Yeah.

Michael Walrath (43:27.256)

and burning tons of money and we were worth five times what we're worth today. So, there, you know, today, you know, you know, if you again, look at sort of the next 12 months consensus and, and then you do the enterprise value, like, you know, you X trades for something like, I don't know, it's four or five times, even. Right. Like, you know, that would, that's like an unheard of multiple, even for a low growth software company, it just, it just is what it is.

Auren Hoffman (43:30.412)

Yeah, crazy. Yeah.

Auren Hoffman (43:52.472)

Totally. Yeah.

Michael Walrath (43:54.616)

Right. And I think, you know, there are always different options that, you know, teams and CEOs can pursue. I, what I try to do is not focus on any of that stuff and focus on if this is a 10 year, 20 year or 30 year time horizon, what, what's the things that I do today to create value in 10 years? that's not always an answer that, that my public shareholders love because, you know, I think in a lot of cases, their business models rely on returns much faster. And I think that's.

You know, the fact that I've been very public and very vocal about that's the lens that I'm going to take. You know, that may cost me some shareholders who are, you know, looking for a faster return.

Auren Hoffman (44:34.318)

And how does someone like you think about, you've got this business, it's not, the business itself is a very good business super problem, we're not really growing. It generates all this cash. So now you go back to your, your, your, your outsiders, like capital allocator hat, you have all this cash coming in and your job now as a money manager to use that cash in an effective way. Like how do you think about that?

Michael Walrath (44:41.543)

Yeah.

Michael Walrath (44:49.122)

Yeah.

Michael Walrath (44:55.618)

Yep. Yeah. so we think I, you know, this is something I talk about all the time internally. and with a board and I talked to our investors about it also, is there's really basically three or four things I can do with that cash. So one is I can just let it pile up on the balance sheet. Right. And then

Auren Hoffman (45:11.82)

Yep. And that is really, it's like, well, maybe I'll come up with the idea later of what to do with it. Or maybe I need a lot more cash to go do something big, like acquiring something or do something big. And gives me some optionality. Yeah. And certainly Berkshire Hathaway does that a lot. Like they have the amount of cash in their balance sheet or Apple or whatever on their balance sheet is just astronomical.

Michael Walrath (45:19.201)

Yeah.

Michael Walrath (45:25.494)

Yeah, totally. Yeah, so I think, you know, the folks.

Michael Walrath (45:34.753)

Yeah. Totally. So I think that's one option and your enterprise value increases on a one -to -one basis, The market generally will value cash at cash. So I think when you don't have anything better to do with it, that's a really good thing to do with it. I think there are at least three other things that...

Auren Hoffman (45:42.168)

Correct. Yeah.

Auren Hoffman (45:51.992)

Sure, it's better than spending it on random stuff. Yeah, yeah.

Michael Walrath (45:56.504)

Well, it's certainly better than spending it on growth that doesn't materialize, right? Because that is the worst thing you can do with it. So there is an element of, you know, as a capital allocation mindset, thinking about like, what is the 10 year DCF valuation of this business look like? If I can accelerate growth through organic investment and be less profitable, and I have really high confidence that I can accelerate growth.

Auren Hoffman (46:00.632)

Correct.

Michael Walrath (46:25.878)

then I would be willing to be less profitable in the short term in order to do that. So that's just organic growth or organic investment in that cash into product initiative, sales, marketing, R &D, things like that. The second thing is obviously &A, right? And so I think in an environment where we have tens of thousands of vertical or smaller software companies who can't raise money for the most part,

Auren Hoffman (46:54.253)

Yeah.

Michael Walrath (46:55.392)

and who are trying to have these sort of existential challenges, there's going to be a robust opportunity for us to grow inorganically through acquisition. And if you do that in a really disciplined way, I think what happens is you can expand the breadth of your offering and you can play into this kind of consolidation theme. So if we buy really smartly at really disciplined prices and

It strategically fits into the thing that our customer wants us to do more of. Then, then it allows us to go in and bundle and package and be far more competitive. There are 10 other great benefits to that sort of thing, which is we unified the data layer. We, know, which, which, which sets the table for, for a generative AI, you know, another form and other types of AI wave and all these other things. So I think strategic and A makes a ton of sense, but it has to be, it has to be very, very disciplined.

Auren Hoffman (47:26.968)

Yep.

Michael Walrath (47:51.958)

when you're dealing with sort of your own currency is much better.

Auren Hoffman (47:56.258)

Yeah, and you're going to want to buy things that are at least break even and then maybe you have ability to grow that EBIT over time unless you're really betting on the growth of that.

Michael Walrath (48:08.982)

Yeah. Well, and that's, that's where I think you just get into a very high risk zone, right? Buying, buying higher growth things that are highly unprofitable puts you into a mode of, know, it's, it's, it's like, it's, it's kind of like saying, Hey, we're going to, yeah. I mean, which by the way, we've, you know, Yex has a history of doing, and we all were on board with it it didn't, and those bets didn't pay off. Right. And they, they came with downside that we have had to, had to execute through. So.

Auren Hoffman (48:20.44)

Could be a bet to company. Yeah.

Michael Walrath (48:34.306)

You know, it's, no different than saying, you know, me, me spending a hundred million dollars on a company that's high growth and, and Bernie cash is really no different than me saying, Hey, I'm going to invest a hundred million dollars of sales and marketing and R and D into a, you know, into a moonshot product offering that may or may not massively accelerate growth. It's the same. It's a capital allocator looks at it the same way. Right. and then the third thing, which is a really useful thing is we, can return that money to shareholders.

in one of two ways, you know, a dividend, which is a very unpopular thing for tech companies to do. Although maybe we'll start to see more of it. Yeah.

Auren Hoffman (49:07.938)

So some of the big ones like Facebook and Microsoft and other ones have done this.

Michael Walrath (49:12.503)

Yeah. Yeah. then, but the more popular certainly and yeah, stock buyback and we've done a lot of this. mean, we repurchased, I think since I've taken over close to 20 million shares, right? Which represents, you know, 15 ish, 15 to 20 % of the company's total share count. We, you know,

Auren Hoffman (49:18.222)

Stock buyback.

Auren Hoffman (49:34.414)

And how do you like, I've seen a lot of companies are doing all these stock buybacks, but then they also are at the same time, you know, issuing a lot of options. And so it's kind of like, it's this weird, it never really works out. you know, the company I was involved with even live ramp, like they did a ton of stock buybacks, hundreds and hundreds of million dollars, but it just never really helped the stock price at all.

Michael Walrath (49:42.166)

Yeah. Yeah.

Michael Walrath (50:00.48)

Yeah, no, well, think so. I think this idea that like the stock buyback actually moves the stock price. It's you know, the rules are designed so that doesn't happen. We can only buy so much of the daily float and like any public company can only buy so much. So you can't really move your stock price, right? I think.

Auren Hoffman (50:14.658)

Yeah. Well, you move it in that over time, there's less shares and potentially those shares are more, especially if the business is doing well, then they all have a greater claim to the future profits essentially.

Michael Walrath (50:30.7)

That's right. Yeah. Well, look, and again, it goes back to what's your lens, right? So with the lens that I ask my team members to think about and really any, know, anyone who owns, who works at Yextone Ownshares is, you know, is you're an owner, right? And so while it might be fun to take that money and like pour it into moonshots, right? Or, you know,

Auren Hoffman (50:34.189)

Yeah.

Auren Hoffman (50:56.28)

Yeah.

Michael Walrath (50:58.264)

The reality is if we take that money and we buy 10 % of our stock back, everybody here now owns 10 % more of the company. Roughly, I'm not a mathematician. That math is probably wrong. It's probably % or something like that. So in order for that math to work, you have to be more than offsetting the dilution of new issuance, which then takes us back to this idea of do you operate efficiently or not?

Auren Hoffman (51:05.55)

Correct. Yeah. 9%. Yeah. Yeah. Yeah. Yeah. Yeah. Yeah. Yeah. Or 11 % depending on which way you go. Yeah. Yeah.

Auren Hoffman (51:23.085)

Yep.

Auren Hoffman (51:28.044)

Yeah, and maybe if less people and, you know, people are valuing different things.

Michael Walrath (51:28.214)

Right. And the more efficiently we operate. Yeah. Yeah. So this thing to me is like a tiramisu, right? It's like, it's like a, what's it was the three color cookie that are that my kids love so much. So like the, the Italian cookies are like red, you know, you got to layer these things on correctly in order to like, in order for them to work, because buying a ton of stock back and then turning around and just issuing a ton more stock, like, you know, yeah, it, offsets some of that dilution.

Auren Hoffman (51:37.453)

Yep.

Auren Hoffman (51:44.098)

Yeah, those are delicious. Yeah.

Yeah.

Michael Walrath (51:58.262)

But like, is that really the best use of that?

Auren Hoffman (52:00.514)

And also, and back in the day, you're kind of like relating everything back to like five years ago. I don't think like the typical investor was thinking about this kind of like dilutive event from issuing all the stock. They were calculating things like growth and EBIT and stuff like that, often without the stock comp. And now I think that's much more common to be using that as part of the calculation.

Michael Walrath (52:26.424)

Yeah, these are, yeah, exactly. These are, these are like really complicated incentive structures, right? Where, you know, it's, it's almost comical, right? Like our financial, I, it boggles my mind how all this, how the, all this stock based accounting, stock based comp accounting works. But, you know, we're paying today. Yeah. All We're, accounting for stock that was issued four years ago at $20 a share as

expense at $20 a share with the stock trading at just over $5 a share today. That's my, look, I, I, is another one I could, could easily screw up, but like my understanding of it is, that the expense that we, that we recognize is based on the price at the time that we issued those shares. So there's this weird thing.

Auren Hoffman (52:56.202)

really? God. OK, that's very complicated. Yeah. Yeah.

Auren Hoffman (53:11.511)

Got it. Okay. And then you then you've got like a four year kind of tail on it.

Michael Walrath (53:16.512)

Yeah, you have like a four year tail because most of those grants are like four year grants. Well, in our case, use RSVs so they're not underwater. They're just worth less than when we granted them. And so you have less incentive, but you're still carrying that cost. So the types of things we just look at it again, and this won't surprise you based on our conversation, we look at issuance dilution, right? So we look at it and we say, well, how much dilution are we actually creating to ourselves and to our shareholders?

Auren Hoffman (53:19.2)

Even if the grants are underwater and no one's ever going to. Or there are issues. Yeah, OK, yeah, yeah, yeah, yeah, OK, got it.

Auren Hoffman (53:31.255)

Yeah.

Auren Hoffman (53:37.56)

Yep.

Michael Walrath (53:44.664)

through all of these different mechanisms. we should be looking, that's another thing when you're generating cash and you have a lot of cash, you should be looking at is like, a lot of our employees look at these incentive structures as part of their compensation. And so they get a share of stock, they sell a share of stock, they're like, that's stock, right? They don't all look at it as a long -term investment. And so we have to look at and figure out, should we be issuing, potentially giving them cash instead of stock because they don't look at it as a long -term investment.

Auren Hoffman (53:57.838)

Of course.

Auren Hoffman (54:01.452)

Yeah. Yeah.

Auren Hoffman (54:10.914)

Yeah, they might value it in a different way. Yeah. Yeah, that makes a lot of sense. This has been amazing. We ask a couple of personal questions. What is a conspiracy theory that you believe?

Michael Walrath (54:18.626)

Okay.

Michael Walrath (54:23.48)

was conspiracy theory that I believe. don't know if this qualifies as a conspiracy theory. and I'm going to say this, you know, broadly, I believe this is completely outside the world of tech. I believe that, our food and healthcare industries in particular, pharmaceutical industries are not necessarily are making us sicker, and, and not nourishing us. And

like outside of the world of tech.

Auren Hoffman (54:53.862)

And they're doing it, they're doing it like, because just the incentives align or is there like somebody in the background actually being like, I want to make people sicker so I can make more money or something. It's like the dentist trying to give you more sugar or something.

Michael Walrath (55:01.662)

Meh, well, yeah.

Yeah, mean, look, I have a really I actually have a really hard time putting intention around these things. think what I think I think, you know, incentives create action. Right. And so, you know, and people, you know, like to eat, you know, stuff that's not good for them. Right. It creates a chemical reaction in their body. Yeah, we all do it. Yeah. Yeah. And so so, know, I wouldn't necessarily call this a conspiracy theory.

Auren Hoffman (55:14.519)

Yeah.

Auren Hoffman (55:25.272)

So I definitely do. I definitely like that. Yeah. Yeah.

Michael Walrath (55:35.732)

from my standpoint, think we just have to, you know, kind of thing. So I guess I'm dodging the question a little bit, but I'm like.

Auren Hoffman (55:42.264)

Was there anything you do on like the health stuff that, you know, is a little bit out there or different or, know, or you think it's going to become more mainstream in the future, but not as mainstream today.

Michael Walrath (55:52.088)

Yeah, well, I mean, so so my wife, who is a great entrepreneur has a I'm to plug her brand here. So this juice I'm drinking is organic, organic crush. She has she has six 100 % organic fast casual restaurants on Long Island, where we where we live for most of the last 20 years. We're Florida residents now. But she she

Auren Hoffman (56:03.168)

Yeah, yeah. Ooh, okay.

Auren Hoffman (56:12.639)

OK.

Michael Walrath (56:20.152)

She, she believes, and I have come to believe over 25 years of her making me smarter that like, you know, so much of the chronic health problems and diseases and things like that, that we face as a country today can be solved through whole foods and whole nutrition. And she's created this incredible brand of, you know, delicious made to order and prepared foods that have no additives, no preservatives, no GMOs, a hundred percent organic.

And it's like, heals people of various elements. and so, yeah, like our life in a lot of ways is built around this idea of like kind of fundamental wholesome, you know, nutrition is actually the cure to a lot of, you know, our problems.

Auren Hoffman (57:04.814)

Okay, interesting. like, one of the things, if you've been like, if you're like a Peter Tia fan and stuff, but he's kind of changed his mind around diet. And he's kind of moved to the where diet is, he thinks it's less important than he used to think. And he's been much more on things like exercise and sleep and other stuff over diet. on your kind of like saying, well, actually, diet is fundamental. It's really important.

Michael Walrath (57:32.248)

I think, yeah, but like what's, I don't know if this is controversial, but what's different about it is that I think, you know, we have gone, so we actually have a, with a great friend of mine, a film production company, we made a movie in 2014 called Fed, or 2010 maybe called Fed Up, which was really a sort of a deep look at kind of the food industry and sugar in particular. And I think one of the things that if you,

you know, over the last 50 or 60 years, most of what we've been told about like what actually is, is nourishing and wholesome is, is largely incorrect. Right. We, we, and, and, you know, our, my philosophy on.

Auren Hoffman (58:13.826)

Yeah, it's, you know, when I was a kid, it was like, instead of butter, let's eat margarine. Like everyone was eating margarine instead of butter.

Michael Walrath (58:18.52)

Yes, totally. Yeah. Yeah. And that all goes back to, mean, have wonkish knowledge of this, but in 1979, the McGovern report came out and we basically said, okay, we're, you know, milk and eggs and meat and, you know, cheese are, are, are bad for us. and so, and over the course of 20 years, basically all of those things got replaced with processed food and sugar and now, and now seed oils, which margarine with seed oils, right.

Auren Hoffman (58:36.237)

Yeah.

Michael Walrath (58:46.742)

And it turns out that actually all of those things, sugar, seed oils, processed food, they are what they create obesity, create diabetes, they create heart disease. And there are these amazing stories now of like, of, no, yeah.

Auren Hoffman (58:51.703)

Okay

Auren Hoffman (59:01.72)

Plus they don't taste as good. mean, just, like, like butter's so tasty. Like it's just always tasted better than margarine. So it's like, we went to the, it was like, it was the worst of all worlds. got like the worst tasting thing for, for, and, worse for you.

Michael Walrath (59:06.828)

Yeah.

Totally.

Michael Walrath (59:15.288)

Yeah, well, the only way to make all that stuff taste good was to dump sugar in it, which we didn't even use sugar. We used high fructose corn syrup. so, I again go back to like, I don't know that there's intention behind this, but I think the evolution of our whole food system over the last 60 years is making us chronically ill. And to break out of that, it's like, go back to your grandparents, right? Like what?

Auren Hoffman (59:18.764)

Yeah, that's true. Good point. Yeah.

Michael Walrath (59:41.112)

Your grandparents ate a lot of red meat and a lot of, I'm not, look, I'm not telling anybody how they should eat. I think all our bodies are different and everyone reacts differently to different things. What I've found is that the more I eat like kind of single ingredient, whole foods in particularly high and things like, you know, meat and, and, and eggs and things like that. I just feel better. I have more energy. I don't have, I'm not always inflamed and you know, that matters at 50 years old, almost almost 50 years old. Like it makes a difference. I know.

Auren Hoffman (59:44.972)

Yeah.

Auren Hoffman (01:00:08.398)

We're getting old.

Michael Walrath (01:00:10.774)

We, ours is the generation that like, you know, sort of we grew up with this, you know, this we're the, we're the, we're the, we're the test case, I think for a lot of this stuff. Yeah.

Auren Hoffman (01:00:20.28)

Totally. Our last question we ask all of our guests, what conventional wisdom or advice do you think is generally bad advice? And you already gave a lot of good ones.

Michael Walrath (01:00:31.426)

Well, yeah, I could just say growth at all costs, but I think we covered that for about an hour. This is a good question. You can edit out my.

Auren Hoffman (01:00:35.791)

Yeah. Totally.

Auren Hoffman (01:00:45.856)

Anything in recruiting you think is like, do you think like there's kind like who you should recruit or how you should recruit or who you should work with or.

Michael Walrath (01:00:53.814)

Yeah, no, that's actually that's a that's a great one. I think the conventional wisdom around what it takes to get things done is is something we need to we need to like seriously question. And and, you know, it's thematically in line with what we've talked about. like, how many people do we need to get things done? How many like we've lost the ability to think in terms of like

leanness, you know, I'd say I'd say we no longer default to any mechanism of, of like, you know, what is the kind of the lean approach to this problem? what and also, you know, we're really good at addition. And we're really bad at portfolio management, right? So so and, you know, we struggle with this inside the company all the time. Well, we need to do this, right?

Auren Hoffman (01:01:25.219)

Yep.

Michael Walrath (01:01:49.6)

And the next question that needs to come up, the next sentence that needs to come out of everyone's mouth is, okay, if we need to do this, if this is the highest priority thing, what gets pushed off the plate? And that goes so much further than just like financial, right? That goes to distraction, that goes to thoughts, that goes to everything else. so I just, like the conventional wisdom is like, there's always an opportunity to add more things to what we're going to do.

Auren Hoffman (01:02:18.221)

Yeah.

Michael Walrath (01:02:18.756)

And, and what we should be doing is, you know, there, there's a time for that, right? There's a time for that when your whole portfolio is performing and you know, you can, you can get better performance by adding more, but this is mostly not that time. so, you know, you, you kind of, you know, ask me for something different. I probably gave you something the same, which I apologize for, but

Auren Hoffman (01:02:40.3)

No, that was great. That was amazing. Thank you, Michael Walroth for joining us on World of DaaS. I follow you at Michael Walroth on LinkedIn. I definitely encourage our listeners to engage with you there. This has been a ton of fun. I really appreciate you coming on the World of DaaS.

Michael Walrath (01:02:55.948)